Term Life Insurance: The Affordable Way to Protect What Matters Most

When you think about protecting your loved ones financially, term life insurance often comes up as one of the most straightforward and affordable ways to do it. Whether you are a new parent, a homeowner with a mortgage, or simply someone who wants to make sure your family is financially secure if the unexpected happens, term life insurance can be a smart move.

But how does term life insurance really work? What does it cover? Is it right for everyone? This post breaks down everything you need to know in simple, practical terms so you can make the right decision for your financial future.

What Is Term Life Insurance

Term life insurance is a type of life insurance that provides coverage for a specific period, or term, typically 10, 20, or 30 years. If you pass away during that term, your beneficiaries receive a tax-free death benefit. If you outlive the term, the policy simply expires unless it is renewed or converted into a permanent policy.

It is life insurance in its purest form. There is no cash value component and no investment features, which is why it is often the most affordable option for getting substantial coverage.

Why Term Life Insurance Could Be the Smart Choice for You

Life is unpredictable, and one of the best ways to protect the people you care about is through life insurance. Term life insurance has grown in popularity for a reason. It offers significant coverage at a lower cost compared to other types of policies, making it an ideal option for anyone who wants to ensure their loved ones are financially secure without overextending their budget.

What makes term life insurance so appealing is its simplicity. Unlike permanent policies that mix insurance with investment or savings components, term life focuses solely on protection. It’s straightforward to understand, easy to manage, and provides peace of mind knowing that your family will be looked after if the unexpected happens.

This type of insurance is particularly valuable during your most financially vulnerable years. Whether you’re raising children, paying off a mortgage, or just starting your career, term life insurance can be tailored to match key stages of your life. It ensures that if something happens to you, your family won’t face financial hardship while still allowing you to stay within your budget.

Why People Choose Term Life Insurance

People choose term life insurance for a variety of reasons. First, it is highly cost effective, offering maximum coverage for minimal premiums. This makes it accessible for young families, first-time homeowners, and anyone looking for straightforward protection.

Term life insurance provides security during critical years. It ensures bills, childcare, and mortgage payments continue even if you are no longer there to cover them.

The simplicity of term life is another big draw. There’s no investment component to worry about, no confusing growth rates or cash value calculations. You know exactly what you’re paying for and what your loved ones will receive.

It’s also versatile. You can tailor the coverage to match key life milestones, such as raising children, paying off a mortgage, or planning for education expenses. Perhaps most importantly, term life gives you peace of mind. You can go about your daily life knowing that if something happens, your family will be taken care of financially.

Different Types of Term Life Insurance

Not all term life policies are the same. Each one is designed to meet different needs and financial goals.

Level term life insurance is the most common option. It provides a fixed death benefit and fixed premiums for the entire term, which makes budgeting simple. This type is ideal for families with steady financial responsibilities who want predictable coverage.

Decreasing term life insurance works differently. Here, the death benefit gradually reduces over time, often aligned with the balance of a mortgage or other debts. Premiums are generally stable or slightly lower than level term, making this a good option if your primary goal is to cover debts that naturally decrease over time.

Renewable term life insurance gives you the flexibility to extend coverage at the end of your term without a medical exam. Premiums will increase with age, but it’s useful if you’re uncertain how long you’ll need protection.

Convertible term life insurance allows you to switch from a term policy to a permanent policy without a medical exam. This flexibility is valuable if your long-term needs change and you decide you want lifelong coverage.

Return of premium term life insurance is a more expensive option, but it refunds your premiums if you outlive the term. It’s ideal for those who want a no-risk savings element along with protection.

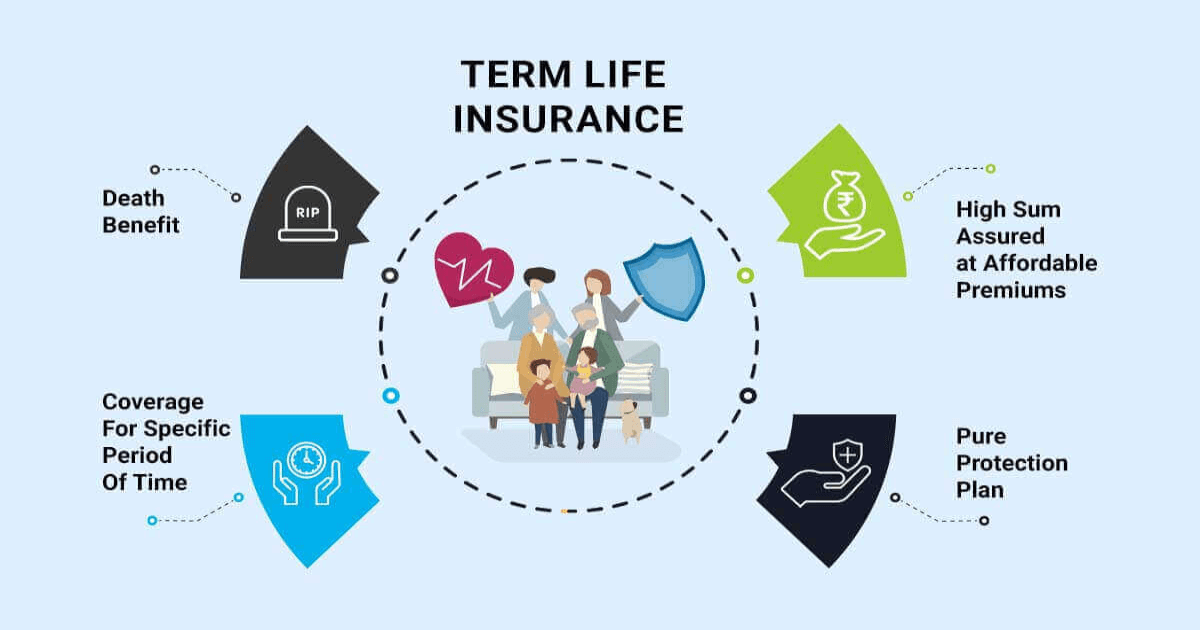

What Term Life Insurance Covers

Term life insurance is designed to provide financial protection for your family. It pays a death benefit to your beneficiaries if you pass away during the coverage period. This benefit can help replace lost income, cover day-to-day living expenses, repay debts, and fund education costs.

Some policies offer additional options, known as riders. These can include coverage for terminal illness or disability, accidental death benefits, or child coverage. These extras give families even more flexibility and protection in the face of life’s uncertainties.

What Term Life Insurance Does Not Cover

It’s equally important to understand what term life insurance does not cover. Most policies do not pay out for suicide within the first two years. Claims can also be denied if the application contains false or incomplete information.

High-risk occupations or hobbies may be excluded if not disclosed at the time of application. Term life also does not build cash value and provides no investment returns. Finally, if you outlive your policy and do not renew it, no payout occurs.

Who Should Consider Term Life Insurance

Term life insurance is not limited to any one group. It’s ideal for anyone seeking affordable, temporary protection. Young families can use it to ensure financial stability while raising children. Homeowners may choose it to cover mortgage obligations. Parents often use term life to fund their children’s education, while breadwinners can provide income replacement for their families. Business owners may also rely on term life to protect key employees or cover loans. It’s particularly useful during high-risk periods of life when you need coverage but don’t want a long-term financial commitment.

How Much Term Life Insurance Do You Need

Finding the right amount of coverage is critical. You want enough to support your loved ones but not so much that it strains your budget. Start by adding up all your current debts, including mortgage, student loans, and credit cards. Estimate the income your family will need over the next ten to twenty years and include future costs like childcare, education, and daily living expenses. Don’t forget final expenses such as funeral costs. Subtract any savings, assets, or other insurance you already have.

A common rule of thumb is to get coverage equal to ten to fifteen times your annual income, but a financial advisor can help refine this number based on your unique situation.

What Affects Term Life Insurance Premiums

Several factors determine how much you will pay for term life insurance. Younger applicants usually pay lower premiums. Your health history, including chronic conditions, blood pressure, and cholesterol, also influences rates. Tobacco use can significantly increase premiums, while certain occupations or hobbies may be considered high risk. The length of your policy and the amount of coverage you choose also impact the cost, with longer terms and higher death benefits generally costing more.

How to Apply for Term Life Insurance

Applying for term life insurance has become simpler thanks to online tools and streamlined processes. Start by determining how much coverage you need and for how long. Compare quotes from multiple providers to find the best rate. Complete your application with accurate health and lifestyle information and take a medical exam if required. Some policies offer no-exam options for faster approval. Once underwriting is complete and your policy is approved, start paying your premiums to activate coverage.

Ways to Save on Term Life Insurance

Protecting your family doesn’t have to break the bank. You can save by purchasing coverage while you are young and healthy, maintaining a healthy lifestyle, and choosing the right term length. Bundling your life insurance with other policies may offer additional discounts. Paying annually rather than monthly can help you avoid extra fees. Shopping around online or using independent brokers can also help you find the best deal for your needs.

Term Life Insurance Compared to Whole Life Insurance

Many people compare term life to whole life insurance. Term life is more affordable and provides temporary coverage, which is ideal for covering specific financial obligations or life stages. Whole life, on the other hand, lasts for your entire life and includes a savings component, but it requires a long-term financial commitment. Term life allows you to buy higher coverage amounts for less money, making it a practical option for families and young professionals who want straightforward protection.

Term life insurance is a flexible, affordable, and practical way to protect the people you love. By understanding your needs, evaluating the types of coverage available, and planning for the future, you can ensure that your family has financial security, even if life doesn’t go according to plan.

Final Thoughts on Term Life Insurance

Term life insurance is one of the most practical and cost-effective ways to protect the people who matter most. It is simple, affordable, and powerful.

Whether you are just starting your family, taking on a mortgage, or building your career, term life coverage can help ensure your loved ones are financially secure if something happens to you. It is not just a policy. It is a promise to protect your family’s future.

Start with a quote. Talk to a licensed agent. Review your options carefully. But most importantly, do not delay. The younger and healthier you are, the easier it is to qualify and lock in great rates. Peace of mind is priceless, and term life insurance is one way to get it.