Life Insurance: Protecting Your Loved Ones and Securing Your Future

Life is unpredictable. One moment, everything feels secure, and the next, an unforeseen tragedy can change everything. While thinking about the end of life is uncomfortable, planning for it is one of the most responsible decisions you can make. That is where life insurance comes in.

Life insurance is not just for the wealthy, the elderly, or those with complicated finances. It is for anyone who has people they love and want to protect. Whether you are a young professional just starting out, a parent managing a household, or a business owner with employees relying on you, life insurance is a critical tool to ensure financial security. In this guide, we will walk through what life insurance is, why it matters, the different types available, and how to choose the right policy for your unique situation.

What Is Life Insurance?

At its core, life insurance is a contract between you and an insurance company. In exchange for regular payments, called premiums, the insurer agrees to pay a lump sum of money, known as a death benefit, to your designated beneficiaries when you pass away. The purpose of this payout is to provide financial security for your loved ones, helping them cover immediate expenses like funeral costs, daily living costs, outstanding debts, and long-term financial goals such as your children’s education or paying off a mortgage.

This security ensures that your family can maintain their standard of living even if the primary breadwinner is no longer there to provide for them. Life insurance acts as a financial cushion, offering protection and stability during one of life’s most difficult moments.

Why Life Insurance Matters

Life today is expensive. Families juggle mortgages or rent, car payments, school fees, rising grocery bills, and credit card balances. Most households rely on two incomes just to make ends meet. Imagine the sudden loss of one income; without life insurance, surviving family members may face serious financial hardship.

Life insurance is more than a financial product. It is a safety net that ensures your family is not left in turmoil after your passing. Its value goes beyond monetary support, it is about protecting your family’s lifestyle, dreams, and future.

Life insurance is essential for several reasons. First, it replaces lost income. Bills, mortgage payments, and everyday expenses do not stop when someone passes away. Life insurance helps families continue to meet these obligations without disruption.

It also pays off debts. Mortgages, car loans, student loans, and other liabilities can become overwhelming if left to surviving family members. Life insurance ensures your loved ones are not burdened with your financial obligations.

Funeral costs are another critical factor. Funerals can cost thousands of dollars, and having coverage means your family will not have to scramble to pay for this final expense.

Beyond immediate expenses, life insurance can support long-term financial goals. It can help fund your children’s education, provide retirement income for your spouse, or cover future household needs, ensuring that your family’s plans continue even after you are gone.

For business owners, life insurance can protect the continuity of operations. Policies can fund buy-sell agreements, protect key partners, and ensure that the business survives financial strain caused by an unexpected loss.

Finally, life insurance provides peace of mind. Knowing that your loved ones will be financially secure allows you to live your life without worry, knowing you have taken steps to protect the people who matter most.

Types of Life Insurance

There is no one-size-fits-all life insurance policy. Different types are designed for different needs and financial goals. Understanding these types is crucial for choosing the right one.

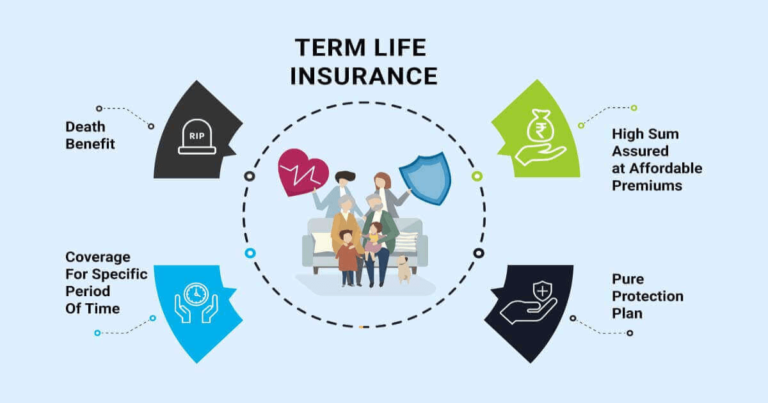

Term Life Insurance is the simplest and often the most affordable. It provides coverage for a specific period, such as 10, 20, or 30 years. If you pass away during this term, your beneficiaries receive the death benefit. Term policies do not accumulate cash value, but they are an excellent choice for young individuals or families who want maximum coverage at a low cost.

Whole Life Insurance offers lifetime coverage as long as premiums are paid. In addition to providing a death benefit, whole life policies include a savings component known as cash value, which grows over time. Premiums are higher than term policies but are fixed and predictable. Policyholders can even borrow against the cash value later in life for emergencies or planned expenses.

Universal Life Insurance provides more flexibility. You can adjust premiums and death benefits as your financial situation changes. It also builds cash value tied to interest rates, making it a versatile option for estate planning and wealth transfer.

Variable Life Insurance combines insurance protection with investment opportunities. Cash value can be allocated to stocks, bonds, or mutual funds, offering growth potential but also increased risk. This type is ideal for financially savvy individuals looking to tie their insurance to long-term investment strategies.

Final Expense Insurance, often called burial insurance, is targeted at seniors. It is affordable, easy to qualify for, and primarily covers funeral and end-of-life expenses.

What Life Insurance Covers

Life insurance is often thought of as a death benefit, but it can offer more. Beneficiaries typically receive a lump sum payout upon the policyholder’s death. Some policies offer accelerated death benefits if the policyholder is diagnosed with a terminal illness, allowing access to funds while still alive. Permanent policies, such as whole life or universal life, let policyholders access cash value for financial needs during their lifetime.

Additional coverage can be added through riders, such as accidental death protection, child protection, or disability benefits. Business owners can also use life insurance to fund buy-sell agreements, insure key employees, or provide business continuity.

What Life Insurance Does Not Cover

It is equally important to understand exclusions. Most policies do not cover suicide within the first two years of the policy. Claims may also be denied if false information is provided on the application or if there is fraud. High-risk activities like skydiving, car racing, or extreme sports can void coverage, and deaths related to war or terrorism often require special riders. Even deaths occurring abroad may have restrictions depending on the insurance provider. Being aware of these exclusions ensures there are no surprises when a claim is needed.

Who Needs Life Insurance

Contrary to popular belief, life insurance is not only for parents with young children. Young professionals may need coverage to pay off student loans or support dependents. Newlyweds often purchase policies to secure their financial future together. Homeowners benefit from life insurance to protect against mortgage debt, while business owners use it to safeguard employees and partners. Seniors may buy smaller policies to cover final expenses or leave a financial legacy, and stay-at-home parents require coverage to replace the value of their household contributions if something unexpected happens.

How Much Coverage Do You Need

Determining the right amount of life insurance coverage is often confusing. A good starting point is to calculate all outstanding debts, including mortgages, loans, and credit cards. Factor in future expenses such as childcare, education, or retirement contributions, and estimate how many years of income your family would need replaced. Don’t forget to include funeral costs. Subtract any savings, investments, or existing coverage already in place. A common guideline is 10 to 15 times your annual income, but a financial advisor can fine-tune this number to fit your unique circumstances.

Factors Affecting Life Insurance Premiums

Life insurance premiums are based on personal and policy-related factors. Age is a primary factor; younger individuals typically pay lower rates. Health history and preexisting conditions can increase costs, while tobacco use almost always results in higher premiums. Occupation and hobbies are considered, especially if they are deemed high-risk. Policy type matters—term insurance is generally less expensive than permanent coverage. Finally, the coverage amount and duration impact premiums, with larger or longer-term policies costing more.

How to Save on Life Insurance

There are practical ways to reduce life insurance costs. Purchasing coverage when you are young and healthy locks in lower rates. Quitting smoking and maintaining good health can also reduce premiums. Term life insurance is typically the most cost-effective option for straightforward coverage. Comparing quotes from multiple providers, considering bundling with home or auto insurance, and paying premiums annually rather than monthly can also save money.

Applying for Life Insurance

Applying for life insurance is simpler than many assume. First, choose the type of policy that fits your needs and estimate the amount of coverage required. Compare quotes from different providers to find the best option. Complete an application, which typically includes questions about your health, lifestyle, and family history. Some policies require a medical exam. Once underwriting is complete and approval is granted, coverage begins immediately after the first premium is paid.

Life Insurance and Estate Planning

Life insurance is a powerful tool for estate planning. Policies can provide liquidity to pay estate taxes, so heirs do not need to sell assets under pressure. Life insurance ensures fair distribution of wealth, supports charitable giving, and can be placed in trusts to control how and when funds are used. For families with complex estates or significant assets, life insurance is an essential component of long-term financial strategy.

Final Thoughts

Life insurance is not about death it is about protection, love, and responsibility. It ensures your children can pursue their education, your spouse can retire comfortably, and your loved ones are not burdened by financial stress. No one knows what tomorrow will bring, but life insurance gives you the power to protect your family today. Whether you opt for term life for affordability or whole life for long-term security, the peace of mind it provides is invaluable.

The best time to secure coverage is now, while you are healthy and insurable. Exploring options and taking the first step toward protecting your family ensures that you are prepared for life’s uncertainties. Life insurance is more than a financial product; it is a promise that your loved ones will be taken care of, no matter what the future holds.